Smart Financial Planning for Beginners: A Step-by-Step Guide to Managing Your Money

Introduction

Many people want to manage their money better, but they do not know where to start. Financial planning may sound complicated, but it is actually very simple when you understand the basic steps.

Smart financial planning means making a clear plan for how you earn, spend, save, and invest your money. When you follow a financial plan, you can avoid money stress and build a secure future for yourself and your family.

The good news is that you do not need to be an expert to start financial planning. Anyone can learn simple money habits that improve financial stability over time.

In this guide, you will learn easy and practical steps that beginners can follow to manage money wisely.

Why Financial Planning Is Important

Financial planning helps you take control of your money instead of letting money problems control your life.

Without a plan, people often spend too much, save too little, and struggle during emergencies. Unexpected expenses such as medical bills, car repairs, or job loss can create serious financial stress.

When you create a financial plan, you prepare for both short-term and long-term goals. It helps you manage daily expenses while also planning for bigger goals like buying a home, starting a business, or retirement.

Financial planning also improves your confidence. When you know where your money goes, you feel more secure and in control.

Step 1: Understand Your Income and Expenses

The first step in financial planning is understanding how much money you earn and how much you spend.

Many people never track their spending, which leads to unnecessary expenses.

Start by writing down all your sources of income. This may include salary, freelance work, business income, or other earnings.

Next, track your monthly expenses. These usually include rent, groceries, utilities, transportation, insurance, and entertainment.

When you see your full financial picture, it becomes easier to identify areas where you can save money.

Small spending habits often add up over time. For example, daily coffee, frequent online shopping, or unused subscriptions can quietly reduce your savings.

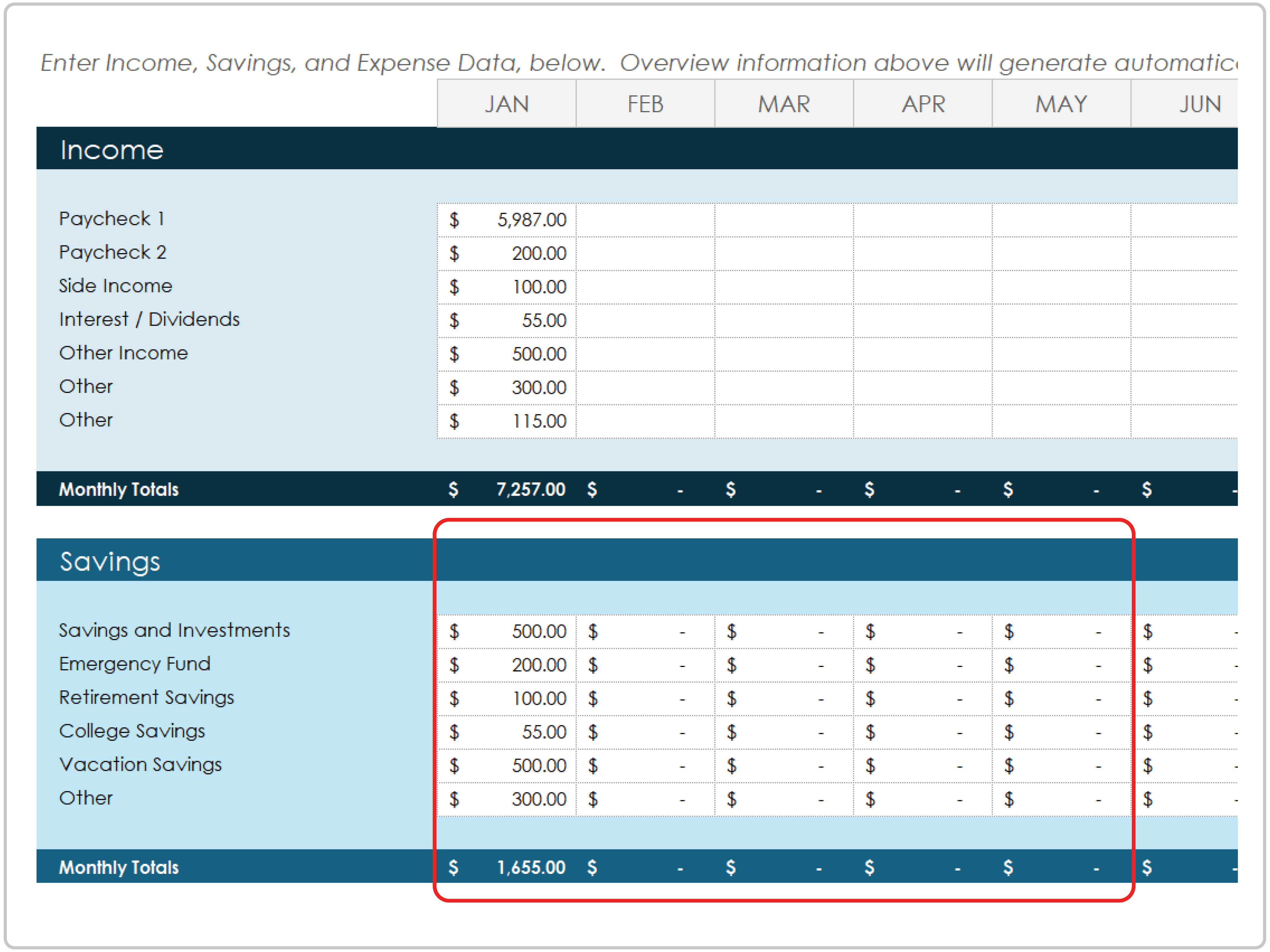

Step 2: Create a Simple Budget

A budget is one of the most powerful tools in financial planning.

A budget helps you control how your money is spent each month. Instead of wondering where your money went, you decide in advance how to use it.

One popular method is the 50-30-20 rule.

In this rule:

50 percent of income goes to necessities like housing, groceries, and bills.

30 percent goes to personal spending such as entertainment, travel, and hobbies.

20 percent goes to savings and investments.

This structure helps maintain balance between enjoying life today and preparing for the future.

Even a simple budget can dramatically improve financial discipline.

Step 3: Build an Emergency Fund

Life is unpredictable. Emergencies can happen anytime.

An emergency fund protects you from financial crises.

Experts recommend saving at least three to six months of living expenses in an emergency fund.

This money should be easily accessible, such as in a savings account.

If saving several months of expenses feels difficult, start small. Even saving a small amount every month will gradually build your emergency fund.

Over time, this financial safety net will reduce stress and help you handle unexpected situations.

Step 4: Reduce and Manage Debt

Debt can become a major obstacle to financial stability.

High-interest debt, especially credit card debt, can grow quickly if not managed carefully.

Start by listing all your debts, including credit cards, personal loans, and other liabilities.

Focus on paying off high-interest debt first. This strategy reduces the total interest you pay over time.

Avoid taking unnecessary loans unless they are for important long-term investments like education or property.

Responsible debt management is a key part of successful financial planning.

Step 5: Start Saving Consistently

Saving money should become a regular habit.

Many people try to save whatever money remains at the end of the month. Unfortunately, that often means saving nothing.

Instead, treat savings as a fixed expense.

Set aside a specific percentage of your income every month. Automating savings through bank transfers can make this process easier.

Consistency is more important than the amount you save.

Even small monthly savings can grow significantly over time.

Step 6: Begin Investing for Long-Term Growth

Saving money protects your finances, but investing helps your money grow.

Inflation slowly reduces the value of money over time. Investments help your money grow faster than inflation.

Beginners can start with simple investment options such as index funds, mutual funds, or retirement accounts.

The key is to start early and invest regularly.

Time plays a powerful role in investing. The longer your money stays invested, the more it can grow through compounding.

Even small investments made consistently can lead to significant financial growth in the future.

Step 7: Set Clear Financial Goals

Financial planning becomes easier when you define clear goals.

Your goals may include:

Buying a house

Starting a business

Traveling the world

Paying for children’s education

Retirement planning

When you have specific goals, it becomes easier to stay motivated and make better financial decisions.

Break large goals into smaller milestones. This makes progress easier to track and maintain.

Step 8: Protect Your Financial Future

Financial protection is often overlooked but extremely important.

Insurance helps protect you and your family from unexpected financial losses.

Health insurance, life insurance, and property insurance can prevent financial disasters.

Although insurance requires monthly payments, it provides valuable protection during difficult situations.

A good financial plan includes both wealth building and risk protection.

Step 9: Continue Learning About Money

Financial education is a lifelong process.

The more you learn about money, the better decisions you can make.

Read books, follow financial blogs, listen to podcasts, or learn from trusted financial experts.

Understanding financial concepts such as investments, taxes, and savings strategies will strengthen your financial future.

Knowledge is one of the most powerful financial tools you can have.

Common Financial Mistakes Beginners Should Avoid

Many beginners make avoidable financial mistakes.

One common mistake is spending more than they earn. Lifestyle inflation often leads to unnecessary financial pressure.

Another mistake is ignoring savings until later in life. The earlier you start saving and investing, the better your results will be.

Some people also rely too much on credit cards without understanding interest rates.

Avoiding these mistakes can significantly improve financial stability.

Conclusion

Financial planning does not have to be complicated.

Simple habits like budgeting, saving consistently, managing debt, and investing early can transform your financial future.

The most important step is simply getting started.

Even small improvements in money management can create powerful long-term results.

When you follow a clear financial plan, you gain control over your finances, reduce stress, and move closer to achieving your life goals.

Financial success is not about earning a huge amount of money. It is about managing the money you have wisely.

Start today, stay consistent, and your financial future will become stronger every year.

Post Comment